Tuesday, November 28, 2006

Misc Update

The price of uranium continues going up. UxC lists the spot price at $63.00, up 50 cents from last week, with the usual increasing nuclear reactor demand news.

ETLT and CXTI have been soaring higher fairly steadily. BKBO is climbing back up. ETLT announced some sort of bamboo farm thing on their website, which doesn't make me happy. I really don't like these odd things they're looking at. I sold some of my ETLT... at a lower price than it's at now. The company has always been a bit close to the boundary of weirdness for me. I think it's worth owning, but I just want to be in a position where if trading halted and bugs crawled out of the woodwork that it wouldn't be terribly damaging. I had bailed out completely back here, but then bought back in 4 days later at a higher price when I found that enough of the red flags were non-issues.

This time, I only sold some of the shares and shifted much of the money into BKBO, which has gone up, but not as much as ETLT. It's the potential price I pay for not worrying so much. I wrote a bit more here.

Strathmore and CXTI are becoming very large holdings percentage-wise, which is fine.

ETLT and CXTI have been soaring higher fairly steadily. BKBO is climbing back up. ETLT announced some sort of bamboo farm thing on their website, which doesn't make me happy. I really don't like these odd things they're looking at. I sold some of my ETLT... at a lower price than it's at now. The company has always been a bit close to the boundary of weirdness for me. I think it's worth owning, but I just want to be in a position where if trading halted and bugs crawled out of the woodwork that it wouldn't be terribly damaging. I had bailed out completely back here, but then bought back in 4 days later at a higher price when I found that enough of the red flags were non-issues.

This time, I only sold some of the shares and shifted much of the money into BKBO, which has gone up, but not as much as ETLT. It's the potential price I pay for not worrying so much. I wrote a bit more here.

Strathmore and CXTI are becoming very large holdings percentage-wise, which is fine.

Monday, November 20, 2006

Strathmore Minerals (STM.V, STHJF) wants a mill and other U news

Strathmore Minerals (combined links) issued this press release.

The stock also went up over 13% today, but that's probably because a big investor seems to think that Cameco's Cigar Lake mine will be delayed by 2 years (the market might be thinking even 2 years is optimistic). And they're thinking uranium prices might go up a lot more.

Getting back to Strathmore Minerals, there is currently only 1 operating uranium mill in the United States (it's in the White Mesa complex in Utah). Strathmore wants to open a mill in the Grants, NM area so they can proceed with a conventional mine (not an in situ mine) to extract a significant portion of the 33 million pounds of uranium ore in an NI 43-101 compliant measured, indicated, and inferred resources.

They bought 650 acres for now (with road and rail access), but they'll also be checking on other areas. They have to jump through a lot of hoops for the Nuclear Regulatory Commission. I'm assuming they'll also need a power generation source or power lines. It's worth noting that these guys are old salts in the business and that can make a big difference in terms of getting stuff done.

If this all works out, then Strathmore will be in the enviable position of having a mine and a mill and 33 million pounds of uranium ore in the ground with the price going to $100 a pound. They'll still need the mining people in perhaps a joint venture, and the mining people and equipment will be in short supply, but so will having a permitted mine and a mill. If Strathmore gets 50% of the profits and it costs $40 per pound fully burdened (I have no idea if this is even close to correct) to mine and mill the ore, this should result in about 25 * .5 * (80 - 40) or about $500 million dollars spread out over a number of years. That assumes extracting 25 million pounds and a selling price of $80 per pound. I had assumed about 100 million totally diluted shares of Strathmore, so that's $5 per share, but must be discounted for time. This is just a guess and a $40 cost of mining and milling could be way off. But I'm betting they'll be able to sell at a significant profit, no?

Of course then there's all the other properties like Athabasca Basin.

The stock also went up over 13% today, but that's probably because a big investor seems to think that Cameco's Cigar Lake mine will be delayed by 2 years (the market might be thinking even 2 years is optimistic). And they're thinking uranium prices might go up a lot more.

Cameco Corp. (CCO CN): RBC Dominion Securities Inc. boosted its uranium price forecast for 2007 to an average of $100 a pound from $55, saying a flood at Cameco Corp.'s Cigar Lake mine in Canada will delay production for two years.Here's their short term plan for how to seal the water leak by pumping concrete into the mine.

Getting back to Strathmore Minerals, there is currently only 1 operating uranium mill in the United States (it's in the White Mesa complex in Utah). Strathmore wants to open a mill in the Grants, NM area so they can proceed with a conventional mine (not an in situ mine) to extract a significant portion of the 33 million pounds of uranium ore in an NI 43-101 compliant measured, indicated, and inferred resources.

They bought 650 acres for now (with road and rail access), but they'll also be checking on other areas. They have to jump through a lot of hoops for the Nuclear Regulatory Commission. I'm assuming they'll also need a power generation source or power lines. It's worth noting that these guys are old salts in the business and that can make a big difference in terms of getting stuff done.

CONCLUSION

If this all works out, then Strathmore will be in the enviable position of having a mine and a mill and 33 million pounds of uranium ore in the ground with the price going to $100 a pound. They'll still need the mining people in perhaps a joint venture, and the mining people and equipment will be in short supply, but so will having a permitted mine and a mill. If Strathmore gets 50% of the profits and it costs $40 per pound fully burdened (I have no idea if this is even close to correct) to mine and mill the ore, this should result in about 25 * .5 * (80 - 40) or about $500 million dollars spread out over a number of years. That assumes extracting 25 million pounds and a selling price of $80 per pound. I had assumed about 100 million totally diluted shares of Strathmore, so that's $5 per share, but must be discounted for time. This is just a guess and a $40 cost of mining and milling could be way off. But I'm betting they'll be able to sell at a significant profit, no?

Of course then there's all the other properties like Athabasca Basin.

Sunday, November 19, 2006

HQ Sustainable Maritime Industries (HQSM) Quick Update

I had looked at HQSM (sec, website) here and here and here (where I said that I still believed it was worth 50 about cents) and finally here in March 2006 (where I didn't say much except that it would probably be worth more than 50 cents).

Ok, so I'll look at the most recent 10-Q:

Period ending Sept 30, 2006.

123 million shares on Sept 30, 2006.

Comparing to Dec 31, 2005, cash is up. Trade receivables are way up. Inventory is up. Net PP&E is down.

519K intangibles.

Loan from related party.

They have a slight amount of net cash, which is a sign of a strong balance sheet.

Revenues are up over 23% from prior year and up over 10% from the prior quarter.

Ok, so why did they need to restate the quarter ending June 30, 2006?

Ok, back to the numbers...

Gross margins are 44% (48% in Q2, 42% in 2005).

Operating margins are 21% (25% in Q2, 16% in 2005).

Net margins are 5.6% due to big finance costs (6.7% in Q2, 12% in 2005 which doesn't have the big finance costs). My first thought is whether these are cash charges or non-cash charges due to changes in stock price and warrants/options.

Cash flow shows the rest of the story.

First of all, the 9 month earnings are a slight loss. Why? In Q1, they said it was due to increased financing costs and bad debt.

Operating cash flow in full year 2005 was negative, despite big earnings due to trade receivables and AP. And that's with a nearly $1 million tailwind from depreciation. In the first 9 months of 2005, it was far worse due to the lack of the $1 million tailwind. Also, in 2005 financing, they issued a lot of stock and paid off bank loans.

Operating cash flow for the first 9 months of 2006 burned up $647K. Again, trade receivables is the big culprit. That's in spite of $3.8 million of non-cash financial and other charges. So in fact, operations have been a big cash drain.

The cash story for 2006 has been that they sell a lot of stuff in exchange for promises. They buy some stuff, including intangibles. And they issue convertible notes to raise $4.2 million to keep the cash flowing.

That story doesn't make me want to buy the stock. Maybe there's something happening in the future that will turn this into a cash generating machine.

Looking at the segment info, I see the same thing I saw before: the fish business still stinks. The other segment is quite profitable. And finance charges are killing the overall bottom line. When you look at the margins and the return on assets in the segments, that's the real story.

In the discussion, they talk about how the net income was greatly affected by non-cash charges, but that's not what I see in the cash flow. How long are those trade receivables going to continue expanding without converting into cash? That's an important factor.

The fish business seems lousy in terms of margins and in terms of return on assets. The company overall currently has a problem generating cash from actual operations rather than financing. Perhaps I'm missing something because this was a quick look. Why did I ever like this stock?

Ok, so now I'll look at the stock price, but it almost doesn't matter. Would I buy it for 10 cents? 5 cents?

Ok, so the ask is under 24 cents. Chart. I'll pass.

UPDATE same day:

I quickly read this this transcript of a conference call from Feb 26, 2006. Lots of happy talk. Lots of "you guys are just so great" questions. The word "cash" occurs exactly twice and both are associated with the same quote:

UPDATE: Nov 23, 2006

I just wanted to make a note for current HQSM investors. I've seen some bashing going on at the Raging Bulls message board. When I toss out a stock as something I won't invest in, that definitely does not mean that I think it's a bad investment, even when I say a lot of bad stuff about it. Many of them are going to be bad, but some of them will probably be outstanding investments, and usually I get a rough sense of how likely that is. The way I filter out stocks, I can guarantee that I'll throw out good investments. I just want to be as sure as I can not to put money into bad investments.

My sense about HQSM is that I don't find it meets my criteria for investing. I think I mentioned elsewhere that if specialty (zero toxin) fish end up being sold in large amounts in the US with reasonably high margins, then HQSM could end up being a good investment. The problem is my confidence level of that happening. When I say that I'd pay X dollars for stock, my intent is to pay a lot less than what I'm confident that it's worth.

Also, other people might have better knowledge than I do about whether it's a good investment or not.

Ok, so I'll look at the most recent 10-Q:

Period ending Sept 30, 2006.

123 million shares on Sept 30, 2006.

Comparing to Dec 31, 2005, cash is up. Trade receivables are way up. Inventory is up. Net PP&E is down.

519K intangibles.

Loan from related party.

They have a slight amount of net cash, which is a sign of a strong balance sheet.

Revenues are up over 23% from prior year and up over 10% from the prior quarter.

Ok, so why did they need to restate the quarter ending June 30, 2006?

The financial statements for the six months and the three months periods ended June 30, 2006 have been restated to reflect the methodology correction for the embedded conversion option of the convertible promissory notes that the Company issued in January 2006. The effective conversion price has been used to measure the intrinsic value of the embedded conversion option under EITF 00-27, the issue 98-5 model.Ok, so it's the same thing that clobbered a lot of Chinese reverse mergers. I've been very happy with how a number of them have been overcoming the accounting issues that were so rampant a year ago. If HQSM can do the same for all the red flags I had about them, then that would make me a lot more comfortable about owning the stock.

Ok, back to the numbers...

Gross margins are 44% (48% in Q2, 42% in 2005).

Operating margins are 21% (25% in Q2, 16% in 2005).

Net margins are 5.6% due to big finance costs (6.7% in Q2, 12% in 2005 which doesn't have the big finance costs). My first thought is whether these are cash charges or non-cash charges due to changes in stock price and warrants/options.

Cash flow shows the rest of the story.

First of all, the 9 month earnings are a slight loss. Why? In Q1, they said it was due to increased financing costs and bad debt.

Operating cash flow in full year 2005 was negative, despite big earnings due to trade receivables and AP. And that's with a nearly $1 million tailwind from depreciation. In the first 9 months of 2005, it was far worse due to the lack of the $1 million tailwind. Also, in 2005 financing, they issued a lot of stock and paid off bank loans.

Operating cash flow for the first 9 months of 2006 burned up $647K. Again, trade receivables is the big culprit. That's in spite of $3.8 million of non-cash financial and other charges. So in fact, operations have been a big cash drain.

The cash story for 2006 has been that they sell a lot of stuff in exchange for promises. They buy some stuff, including intangibles. And they issue convertible notes to raise $4.2 million to keep the cash flowing.

That story doesn't make me want to buy the stock. Maybe there's something happening in the future that will turn this into a cash generating machine.

Looking at the segment info, I see the same thing I saw before: the fish business still stinks. The other segment is quite profitable. And finance charges are killing the overall bottom line. When you look at the margins and the return on assets in the segments, that's the real story.

In the discussion, they talk about how the net income was greatly affected by non-cash charges, but that's not what I see in the cash flow. How long are those trade receivables going to continue expanding without converting into cash? That's an important factor.

CONCLUSION

The fish business seems lousy in terms of margins and in terms of return on assets. The company overall currently has a problem generating cash from actual operations rather than financing. Perhaps I'm missing something because this was a quick look. Why did I ever like this stock?

Ok, so now I'll look at the stock price, but it almost doesn't matter. Would I buy it for 10 cents? 5 cents?

Ok, so the ask is under 24 cents. Chart. I'll pass.

UPDATE same day:

I quickly read this this transcript of a conference call from Feb 26, 2006. Lots of happy talk. Lots of "you guys are just so great" questions. The word "cash" occurs exactly twice and both are associated with the same quote:

You have good cash on hand. You reported that revenues for the nine months ending September 2005, which is your last quarter report, rose by 115% from 2004, the period before, and that third quarter profit from operations was up 22%. Now that you've just passed your year-end. Do you care to comment on what we might see in that last quarter and could you possibly give us some guidance for 2006?The first sentence is oddly unrelated to the rest of the question. This isn't someone seeking information for making [possible] future investment decisions, it's someone looking for confirmation of a previous investment decision.

UPDATE: Nov 23, 2006

I just wanted to make a note for current HQSM investors. I've seen some bashing going on at the Raging Bulls message board. When I toss out a stock as something I won't invest in, that definitely does not mean that I think it's a bad investment, even when I say a lot of bad stuff about it. Many of them are going to be bad, but some of them will probably be outstanding investments, and usually I get a rough sense of how likely that is. The way I filter out stocks, I can guarantee that I'll throw out good investments. I just want to be as sure as I can not to put money into bad investments.

My sense about HQSM is that I don't find it meets my criteria for investing. I think I mentioned elsewhere that if specialty (zero toxin) fish end up being sold in large amounts in the US with reasonably high margins, then HQSM could end up being a good investment. The problem is my confidence level of that happening. When I say that I'd pay X dollars for stock, my intent is to pay a lot less than what I'm confident that it's worth.

Also, other people might have better knowledge than I do about whether it's a good investment or not.

However, cod fish egg pasta sauce, that's a different story. Tarako!

Thursday, November 16, 2006

Shades of Pink

Pink Sheets LLC is doing something I consider to be a brilliant idea. On the surface, it's very simple: they're introducing different categories for companies traded on the Pink Sheets. Since Pink Sheets does not have minimum disclosure standards like the other exchanges like NASDAQ, they're taking the regulation into their own hands.

OTCQX: Top of the line listing, reserved for substantial operations with proper credible disclosure. About 20% of the stocks should have this classification. This requires filing an application to agree to follow reporting standards.

Emerging Equities List: credible disclosure, audited GAAP financials, although they might not have full qualifications for the other exchanges. This requires filing an application to agree to follow reporting standards.

SEC Current: Up to date with SEC filings.

Adequate Current Information: An audit is not needed, but a letter from an attorney regarding completeness of disclosure is needed. Also, formal regulatory filings with entities like presumably FDIC and such are good enough.

Limited Information Available: Some information is posted in the last 6 months, but might not be current or complete.

Public Interest Concern: "stocks with unsolicited spam, questionable promotion or other public-interest concerns. A Skull and Crossbones icon will be displayed next to the symbol." Quotes can be blocked if there's not current info available.

No Information: Everything else. A "stop sign" is used for these.

I believe this is an outstanding move by Pink Sheets and is exactly what is needed: SEC-Lite.

UPDATE Nov 19, 2006:

I'd like to answer the [first] comment to this post about why I add the seemingly weird comments (and presumably the off-topic videos/pictures/links) like the one below about Milton Friedman.

Very often I will mention things that I consider to be important--to me at least--or else just weird interesting stuff that I find, such as a tiger staring at an ice cream cone, which to me is interesting for a number of intellectual reasons such as how it relates to the book Thinking in Pictures. Sometimes, I just post something funny or silly. Sometimes, it's one of those things that just profoundly messes up my mental model of how things work. Most people don't click on the off-topic links and I don't expect most of them to. But I know for myself, I've discovered a lot of interesting things from casual links I've found on other website and blogs. I tend to be one of those people that will do a huge amount of web crawling around a particular topic. I've found this often results in finding other interesting things that I had never known about. I've spent a good part of my life learning about all sorts of useless things such as the history of the paperclip, which is actually an interesting example of market evolution. I typically find these off-the-beaten-path areas of knowledge in side notes, off-topic links, or just a mysterious mention somewhere without any further explanation.

I consider Milton Friedman to be one of the greatest economists since Adam Smith. Friedman was a great champion for economic freedom. He was arguably a major contributor to why the US economy has been run so well in the past 25 years. During that time, we've had two opportunities to dive into a Great Depression or a 1970s style stagflation tar pit and we've passed through them surprisingly well.

Trading is driven by OTC market demand rather than the traditional exchange listing process. Therefore, categorizing securities by their level of disclosure will greatly enhance the capital formation process. The categories are based on the level, quality and timeliness of a company's disclosure. The initiative is similar to the various markets that NASDAQ uses to classify companies as well as the identifiers that NASDAQ and NYSE use to label companies that are late or delinquent in disclosure. Pink Sheets will implement the new categories on May 1, 2007.

OTCQX: Top of the line listing, reserved for substantial operations with proper credible disclosure. About 20% of the stocks should have this classification. This requires filing an application to agree to follow reporting standards.

Emerging Equities List: credible disclosure, audited GAAP financials, although they might not have full qualifications for the other exchanges. This requires filing an application to agree to follow reporting standards.

SEC Current: Up to date with SEC filings.

Adequate Current Information: An audit is not needed, but a letter from an attorney regarding completeness of disclosure is needed. Also, formal regulatory filings with entities like presumably FDIC and such are good enough.

Limited Information Available: Some information is posted in the last 6 months, but might not be current or complete.

Public Interest Concern: "stocks with unsolicited spam, questionable promotion or other public-interest concerns. A Skull and Crossbones icon will be displayed next to the symbol." Quotes can be blocked if there's not current info available.

No Information: Everything else. A "stop sign" is used for these.

I believe this is an outstanding move by Pink Sheets and is exactly what is needed: SEC-Lite.

"Companies are known by the company they keep, and we hope that in providing these new categories, companies that provide disclosure to the public will clearly stand apart from those companies that are of lesser quality," concluded Mr. Coulson.

UPDATE Nov 19, 2006:

I'd like to answer the [first] comment to this post about why I add the seemingly weird comments (and presumably the off-topic videos/pictures/links) like the one below about Milton Friedman.

Very often I will mention things that I consider to be important--to me at least--or else just weird interesting stuff that I find, such as a tiger staring at an ice cream cone, which to me is interesting for a number of intellectual reasons such as how it relates to the book Thinking in Pictures. Sometimes, I just post something funny or silly. Sometimes, it's one of those things that just profoundly messes up my mental model of how things work. Most people don't click on the off-topic links and I don't expect most of them to. But I know for myself, I've discovered a lot of interesting things from casual links I've found on other website and blogs. I tend to be one of those people that will do a huge amount of web crawling around a particular topic. I've found this often results in finding other interesting things that I had never known about. I've spent a good part of my life learning about all sorts of useless things such as the history of the paperclip, which is actually an interesting example of market evolution. I typically find these off-the-beaten-path areas of knowledge in side notes, off-topic links, or just a mysterious mention somewhere without any further explanation.

{kind=link}

I consider Milton Friedman to be one of the greatest economists since Adam Smith. Friedman was a great champion for economic freedom. He was arguably a major contributor to why the US economy has been run so well in the past 25 years. During that time, we've had two opportunities to dive into a Great Depression or a 1970s style stagflation tar pit and we've passed through them surprisingly well.

Rest in Peace, Milton Friedman

Wednesday, November 15, 2006

The market goes wild

CXTI (links) up 42.04% today

ETLT (links) up 28.27% today

Strathmore Minerals (links) up 6.85% today

My three largest holdings. All three are doing great in terms of value and now in terms of market price. [UPDATE: Note that 99% of the other days, these stocks did much, much worse. And I expect the future to be more like the other 99%.]

Strathmore announced that they might have found some uranium, which doesn't mean much until they get more work done on it. Also, the spot price of uranium jumped up another $2.50 to $62.50. UxC also put up two presentation pdf files (here and here) from the Quebec session recently, which are somewhat interesting. The best part is the color coded uranium market conditions similar to the terrorist threat color coding. They go from "RED - Supplies are so scarce that reactors are in danger of shutting down" to the very humorous "GREEN - There is no way a uranium salesman would beat you in a game of golf."

And CVU (links) released what I consider to be somewhat good news: press release, 10-Q. The results are bad, but not as bad as they've been. And things are looking up for the future.

UPDATE same day:

An anonymous person wrote a comment in the previous post which said,

"These results are very convincing.

It is just totally undiscovered I guess.

Agree that E sea was acquistion of the century. If they can repeat that then this really is a five buck stock on a low PE...not sure about turtles though

"Must be many shareholders who have held for months if not years and want out. Saw a very healthy volume today at close to 10% of freefloat shares not under control of management.....should go higher IMHO"

I think there's some interesting evidence supporting the "undiscovered" theory. While Yahoo automatically generated this news item Tuesday at 5:09 PM EST when the 10-Q was posted, the real trading volume today happened after ETLT issued the press release around noon today (the next day). Unfortunately, you can't see it easily because someone painted the tape with a 4 billion share trade just after 2:00 PM. Haha, very funny. But you can see the result in the price chart for the day. Nothing really happened until noon. Then, BANG! it took off.

If lots of people were following this very closely, they would have known about the results before the opening. I bought some more shares with some new extra cash just after the open, only the see the price deflate to under 50 cents during the morning.

I have no idea what the stock will do over the next weeks or months. But I'd be surprised if it just sinks back down again. The accounting issues are cleared up. The mysterious things are gone. Someone must have bought them a calculator. :-) The 10-Q was filed on time. And the results are outstanding. It's hard to believe the stock is under a dollar, but then I sat on ValueClick selling under net cash value (and making a profit) for what seemed like an amazing amount of time before people were willing to go back into the water when it was OK be own an Internet advertising stock again. (I stupidly bailed out at around $4.40 and it's $22.13 now, a missed 10-bagger)

ETLT (links) up 28.27% today

Strathmore Minerals (links) up 6.85% today

My three largest holdings. All three are doing great in terms of value and now in terms of market price. [UPDATE: Note that 99% of the other days, these stocks did much, much worse. And I expect the future to be more like the other 99%.]

Strathmore announced that they might have found some uranium, which doesn't mean much until they get more work done on it. Also, the spot price of uranium jumped up another $2.50 to $62.50. UxC also put up two presentation pdf files (here and here) from the Quebec session recently, which are somewhat interesting. The best part is the color coded uranium market conditions similar to the terrorist threat color coding. They go from "RED - Supplies are so scarce that reactors are in danger of shutting down" to the very humorous "GREEN - There is no way a uranium salesman would beat you in a game of golf."

And CVU (links) released what I consider to be somewhat good news: press release, 10-Q. The results are bad, but not as bad as they've been. And things are looking up for the future.

Third quarter revenue, while down from the same period last year, was 80% ahead of the 2006 second quarter’s $2.5 million. Included in the third quarter revenue was approximately $1.0 million that we were unable to record in the preceding quarter due primarily to supplier delays. Gross margin has improved as compared to the second quarter of 2006. We expect that gross margin will continue to improve and return to our historically normal rate of approximately 30% during 2007. The staff reductions that we made at the end of the second quarter have helped to lower overhead and have contributed to our improved gross margin, and the supplier issues which caused us to incur significant overtime and rework costs are essentially behind us.and

We are reporting 2007 guidance at this early stage because of the significant increase in revenue and net income that we project for 2007. We do not expect to report guidance this early in future years. Based upon the level of new and pending orders, we are anticipating 2007 revenue to be approximately $25 million, with a resulting net income of approximately $2.0 million.I need to do a detailed post on their results, but the only things that matter are that they can get through the current slow period and that things will pick up significantly in the future.

UPDATE same day:

An anonymous person wrote a comment in the previous post which said,

"These results are very convincing.

It is just totally undiscovered I guess.

Agree that E sea was acquistion of the century. If they can repeat that then this really is a five buck stock on a low PE...not sure about turtles though

"Must be many shareholders who have held for months if not years and want out. Saw a very healthy volume today at close to 10% of freefloat shares not under control of management.....should go higher IMHO"

I think there's some interesting evidence supporting the "undiscovered" theory. While Yahoo automatically generated this news item Tuesday at 5:09 PM EST when the 10-Q was posted, the real trading volume today happened after ETLT issued the press release around noon today (the next day). Unfortunately, you can't see it easily because someone painted the tape with a 4 billion share trade just after 2:00 PM. Haha, very funny. But you can see the result in the price chart for the day. Nothing really happened until noon. Then, BANG! it took off.

If lots of people were following this very closely, they would have known about the results before the opening. I bought some more shares with some new extra cash just after the open, only the see the price deflate to under 50 cents during the morning.

I have no idea what the stock will do over the next weeks or months. But I'd be surprised if it just sinks back down again. The accounting issues are cleared up. The mysterious things are gone. Someone must have bought them a calculator. :-) The 10-Q was filed on time. And the results are outstanding. It's hard to believe the stock is under a dollar, but then I sat on ValueClick selling under net cash value (and making a profit) for what seemed like an amazing amount of time before people were willing to go back into the water when it was OK be own an Internet advertising stock again. (I stupidly bailed out at around $4.40 and it's $22.13 now, a missed 10-bagger)

Eternal Technologies (ETLT) files Q3 report on time!

ETLT (combined links) filed their 10-Q report on time. That alone is big news.

Period ending Sept 30, 2006 (also looking at Q2):

40,567,300 shares on Nov 14, 2006, exactly the same as Q2.

Balance Sheet

Cash and short term investments are $40.2 millon vs $37.2 million in Q2. (Renminbi restrictions apply)

Accounts receivable climbs back up to $2.4 million from under $1 million (but down from more than $7 million at the end of last year).

Net cash and short term investments is $37 million or over 91 cents per share.

Book value is $53.3 million ($1.31 per share), up from $50.9 million in Q2.

The numbers all add up correctly! (yeah, that's a very low hurdle, but then again....)

Income Statement

Revenues $7.1 million (up from $5.0 million last year, but down from $10.4 million in Q2 although it's largely seasonal).

45% gross margin

27.8% operating margin

12% tax rate on operating income

26% net margin!

5 cents earned per diluted share (slightly over 10 cents so far this year)

Again, the numbers add up correctly (it's sad to actually need to check).

Cash Flow

9 month cash flow from operations is screaming at $11.2 million due to AR and AP.

Capex is zero so far this year!

No financing.

The only other significant cash flow is the purchase of short term investments of $15 million.

Free cash flow is $11 million (27 cents per share).

Plus $828K tailwind from currency translaton benefits.

Again, the numbers add up correctly.

Notes

No related party transactions this year.

Management's Discussion

E-Sea's revenues increased to $3.70 million in Q3 from $2.06 [oops, that's $1.46 million] in Q2, a 79% [no, it's 154%] increase! E-Sea's operating income is $1.68 million up 57% from Q2's $945K! E-Sea total assets increased to $7.74 million from $5.99 million. Their returns on assets are simply amazing.

[see Note 8. Segment Reporting, notice that it's year-to-date]

When you take the $1.68 million in E-Sea operating income for Q3 and subtract the $69K of depreciation associated with E-Sea and the $253K taxes for E-Sea listed in the Mgmt Discussion, you end up with $1.36 million net earnings from E-Sea alone for Q3, which is 3.35 cents per share which alone would justify a stock price of at least $2.00, not even counting the net cash (and short term investments) of 91 cents per share.

In Segment Reporting, the agribusiness operating margins are 11%, down from 22% last year's Q3.

Roll mutton sales are up, cattle embryo transfers and lamb meat (high margin) sales are down.

No internal control changes.

No changes in legal stuff (same small pending lawsuits).

These results... what's the phrase I'm looking for here... um... kick ass!

SEC filing on time... check

Numbers add up... check

No funny business or weirdness... check

Net cash/short term investments... 91 cents per share

Book value... $1.31 per share

E-Sea earnings alone... 3.35 cents per share for Q3

Overall earnings... 5 cents per share for Q3

Nine month free cash flow... 27 cents per share

Current stock price... less than 47 cents

Yeah, I think I'm gonna hang onto the the shares I own.

UPDATE same day:

lionsshare1 over on the Raging Bulls message board points out that my E-Sea revenue increase was wrong. It was too low. I had taken the 9 month results and subtracted the 3 month results from them, comparing Q3 against Q1+Q2 rather than just Q2. The actual results were even better.

Period ending Sept 30, 2006 (also looking at Q2):

40,567,300 shares on Nov 14, 2006, exactly the same as Q2.

Balance Sheet

Cash and short term investments are $40.2 millon vs $37.2 million in Q2. (Renminbi restrictions apply)

Accounts receivable climbs back up to $2.4 million from under $1 million (but down from more than $7 million at the end of last year).

Net cash and short term investments is $37 million or over 91 cents per share.

Book value is $53.3 million ($1.31 per share), up from $50.9 million in Q2.

The numbers all add up correctly! (yeah, that's a very low hurdle, but then again....)

Income Statement

Revenues $7.1 million (up from $5.0 million last year, but down from $10.4 million in Q2 although it's largely seasonal).

45% gross margin

27.8% operating margin

12% tax rate on operating income

26% net margin!

5 cents earned per diluted share (slightly over 10 cents so far this year)

Again, the numbers add up correctly (it's sad to actually need to check).

Cash Flow

9 month cash flow from operations is screaming at $11.2 million due to AR and AP.

Capex is zero so far this year!

No financing.

The only other significant cash flow is the purchase of short term investments of $15 million.

Free cash flow is $11 million (27 cents per share).

Plus $828K tailwind from currency translaton benefits.

Again, the numbers add up correctly.

Notes

No related party transactions this year.

Management's Discussion

E-Sea's revenues increased to $3.70 million in Q3 from $2.06 [oops, that's $1.46 million] in Q2, a 79% [no, it's 154%] increase! E-Sea's operating income is $1.68 million up 57% from Q2's $945K! E-Sea total assets increased to $7.74 million from $5.99 million. Their returns on assets are simply amazing.

[see Note 8. Segment Reporting, notice that it's year-to-date]

When you take the $1.68 million in E-Sea operating income for Q3 and subtract the $69K of depreciation associated with E-Sea and the $253K taxes for E-Sea listed in the Mgmt Discussion, you end up with $1.36 million net earnings from E-Sea alone for Q3, which is 3.35 cents per share which alone would justify a stock price of at least $2.00, not even counting the net cash (and short term investments) of 91 cents per share.

In Segment Reporting, the agribusiness operating margins are 11%, down from 22% last year's Q3.

Roll mutton sales are up, cattle embryo transfers and lamb meat (high margin) sales are down.

No internal control changes.

No changes in legal stuff (same small pending lawsuits).

CONCLUSION

These results... what's the phrase I'm looking for here... um... kick ass!

SEC filing on time... check

Numbers add up... check

No funny business or weirdness... check

Net cash/short term investments... 91 cents per share

Book value... $1.31 per share

E-Sea earnings alone... 3.35 cents per share for Q3

Overall earnings... 5 cents per share for Q3

Nine month free cash flow... 27 cents per share

Current stock price... less than 47 cents

Yeah, I think I'm gonna hang onto the the shares I own.

UPDATE same day:

lionsshare1 over on the Raging Bulls message board points out that my E-Sea revenue increase was wrong. It was too low. I had taken the 9 month results and subtracted the 3 month results from them, comparing Q3 against Q1+Q2 rather than just Q2. The actual results were even better.

Tuesday, November 14, 2006

China Expert Technology (CXTI) Q3 and new contract

CXTI (combined links) released their 10-Q today and also a new contract award. They also had a conference call, but I'll get to that later.

First, the 10-Q (and comparing it to Q2):

Period ending Sept 30, 2006.

29 million shares on Sept 30, 2006. Add about 10 million to that for warrants and subsequent issued stock.

On the balance sheet, total assets increased by $8 million from Q2. This is mostly due to earnings, but also a drop in derivatives and warrants due to a drop in the stock price, and also $2.8 million additional paid-in capital (probably convertibles and warrants).

Cash jumped to $22.5 million from $13.0 million. $2.7 million net cash (i.e. strong balance sheet).

AR dropped to $21.5 million from $25.4 million.

Revenue up by all measures due to a bunch of contracts starting up.

Gross margins up to 52.0% (6.7% increase from prior year). Due to a higher mix of training and system maintenance, less subcontracting. See press release and results of operations in 10-Q (page 27).

$120 million cost and estimated earnings so far.

$115 million billed to customers.

Revenues:

Another huge "advertising" charge due to paying [in 1.1 million shares] what seems like essentially a sales commission for the ShiShi City contract. Considering that we would view the stock as cheap (otherwise we wouldn't own it), this seems like a huge payment.

Also a $1 million hit to earnings due to the liquidation damages covered in the previous CXTI post. Caused G&A jump to $1.2 million from $834K in Q2.

Despite all this, operating income increased over 100% from the prior year, although it was down from Q2.

Q3 operating income: $5.9 million

Q2 operating income: $6.4 million

Operating cash flow is greatly helped by the use of stock for currency, offset totally by the large increase in AR and estimated earnings in excess of billings. In reality, they didn't generate much cash from actual operations this year so far. I've said before that this is the nature of this business. It eats cash up front with long cycles. It's bad, but the nature of the business.

Capex is tiny again. In financing, they [net] repaid some money to a former officer. $1 million is due from Mr. Lai Man Yuk. $1.5 million is due to Mr. Lai Man Yuk. The 10-Q has the details of the rental agreement and intended acquisition.

There's $11.8 million in purchase obligations for agreements with subcontractors on page 33 due in less than one year.

Sept 15, 2006 legal issue with Montauk who's seeking $600K. I've covered it before.

Jan 10: 33K shares paid to debenture investors for interest

Jan 25: 1.2 million shares paid to consultant for winning Licheng City contract.

Apr 19: 31K shares paid to 3 [of 5] debenture investors for interest

June 8: 19K shares paid to 2 debenture investors (yeah yeah, I hope I remember it's two next time) for interest

July 11: 43K shares issued for interest

July 17: 1.1 million shares paid to consultant for winning ShiShi City contract (page 28) (I hope these aren't kickbacks, it says independent consultant...)

The total charged against income for these two big blocks of stock is around $5.5 million. That's a lot to pay for sales commission.

Feb 11: 150K warrants issued ($1.08 strike, 5 years) for consultant services.

Total of 6.6 million warrants outstanding, about 2 million have a strike of $3.06.

Oct 4: 44K shares issues for interest

Oct 31: 614 shares being paid to debenture holders

In Q2, the changes in value of derivatives caused a $3.8 million charge. In Q3, the changes boosted results up by $2.2 million. This makes net income meaningless from my perspective, which is why I don't like this method of accounting for the cost of the convertibles and warrants. But it's not like I have anything else that could be used.

If you average out the net income of the last two quarters, it becomes a lot more meaningful at around $3.2 million per quarter (making sure not to count the currency translation gains, which I believe will continue for some time). In my Q2 notes, I assumed 50 million totally diluted shares (this seems pessimistic). So by my own strange flavored accounting, I'd say they're earning around 6.4 cents per totally diluted share per quarter. If you annualize it and slap a P/E of 15 onto it, you'd get $3.84. I figure the stock is probably worth at least $4.00 per share.

I continue to own the stock.

First, the 10-Q (and comparing it to Q2):

Period ending Sept 30, 2006.

29 million shares on Sept 30, 2006. Add about 10 million to that for warrants and subsequent issued stock.

On the balance sheet, total assets increased by $8 million from Q2. This is mostly due to earnings, but also a drop in derivatives and warrants due to a drop in the stock price, and also $2.8 million additional paid-in capital (probably convertibles and warrants).

Cash jumped to $22.5 million from $13.0 million. $2.7 million net cash (i.e. strong balance sheet).

AR dropped to $21.5 million from $25.4 million.

Revenue up by all measures due to a bunch of contracts starting up.

Gross margins up to 52.0% (6.7% increase from prior year). Due to a higher mix of training and system maintenance, less subcontracting. See press release and results of operations in 10-Q (page 27).

$120 million cost and estimated earnings so far.

$115 million billed to customers.

Revenues:

Specifically, during the third quarter the Company recognized revenue from the 3rd and 4th Phases of Jinjiang, including systems and application training and maintenance contracts, the 3rd and 4th Phases of Dehua, the 1st and 2nd Phases of Nan'an and Huian.Backlog (including the new contract today) is $119.2 million, down from $125.7 million in August. Page 25 has the table of contracts. ShiShi City is $37 million and it's just starting now. There's a gigantic contract for $31.2 million in "Licheng" starting Nov 2006 and ending Oct 2009. Nan'an has $15.2 million remaining (just started), and Huian has $9.7 million remaining (started this year). Most everything else is small.

Another huge "advertising" charge due to paying [in 1.1 million shares] what seems like essentially a sales commission for the ShiShi City contract. Considering that we would view the stock as cheap (otherwise we wouldn't own it), this seems like a huge payment.

Also a $1 million hit to earnings due to the liquidation damages covered in the previous CXTI post. Caused G&A jump to $1.2 million from $834K in Q2.

Despite all this, operating income increased over 100% from the prior year, although it was down from Q2.

Q3 operating income: $5.9 million

Q2 operating income: $6.4 million

Operating cash flow is greatly helped by the use of stock for currency, offset totally by the large increase in AR and estimated earnings in excess of billings. In reality, they didn't generate much cash from actual operations this year so far. I've said before that this is the nature of this business. It eats cash up front with long cycles. It's bad, but the nature of the business.

Capex is tiny again. In financing, they [net] repaid some money to a former officer. $1 million is due from Mr. Lai Man Yuk. $1.5 million is due to Mr. Lai Man Yuk. The 10-Q has the details of the rental agreement and intended acquisition.

There's $11.8 million in purchase obligations for agreements with subcontractors on page 33 due in less than one year.

Sept 15, 2006 legal issue with Montauk who's seeking $600K. I've covered it before.

Jan 10: 33K shares paid to debenture investors for interest

Jan 25: 1.2 million shares paid to consultant for winning Licheng City contract.

Apr 19: 31K shares paid to 3 [of 5] debenture investors for interest

June 8: 19K shares paid to 2 debenture investors (yeah yeah, I hope I remember it's two next time) for interest

July 11: 43K shares issued for interest

July 17: 1.1 million shares paid to consultant for winning ShiShi City contract (page 28) (I hope these aren't kickbacks, it says independent consultant...)

The total charged against income for these two big blocks of stock is around $5.5 million. That's a lot to pay for sales commission.

Feb 11: 150K warrants issued ($1.08 strike, 5 years) for consultant services.

Total of 6.6 million warrants outstanding, about 2 million have a strike of $3.06.

Oct 4: 44K shares issues for interest

Oct 31: 614 shares being paid to debenture holders

In Q2, the changes in value of derivatives caused a $3.8 million charge. In Q3, the changes boosted results up by $2.2 million. This makes net income meaningless from my perspective, which is why I don't like this method of accounting for the cost of the convertibles and warrants. But it's not like I have anything else that could be used.

If you average out the net income of the last two quarters, it becomes a lot more meaningful at around $3.2 million per quarter (making sure not to count the currency translation gains, which I believe will continue for some time). In my Q2 notes, I assumed 50 million totally diluted shares (this seems pessimistic). So by my own strange flavored accounting, I'd say they're earning around 6.4 cents per totally diluted share per quarter. If you annualize it and slap a P/E of 15 onto it, you'd get $3.84. I figure the stock is probably worth at least $4.00 per share.

I continue to own the stock.

Sunday, November 12, 2006

Results 3

Previous Results:

5/28/2006 Checking back with Mr. Market: 1

BFTC, LIAL, LCLG, BRSI, BSOG, BAYN, RCBK, CNB, CFNA, WTFC, Pacific International Bank, BGII, BLYM, AMEN, BVBC, BNSIA, BOGN, BONL, BAWC, BWTL, BPTR, BDLF, BLLD, BURCA, LVWD, BKBO, BOJF, SCCB

5/29/2006 Checking back with Mr. Market: 2

BUKS, XAIN, YIWA, SHFK, SODI, YHGG

10/13/2006 Results 1

BFTC, BKBO, LVWD, LCLG, BRSI, BSPA, BSOG, BOJF, BAYN (Oops, I already did these!)

10/21/2006 Results 2

ADY, BABB, BACL, CACC

New Results:

CBBT (now CBAK, sec)

First looked at it here. My notes only say that it wasn't cheap at the time. It's selling today for around the same price: $6.66.

Here's something you don't see very often: stock options cancelled at the request of the employees.

So far, I'd say that I called this one reasonably well (although the stock is down because they've had a bigger than expected slowdown).

Grade: B

CAPS (stock, sec)

First looked at it here. Neutralizing medical waste into normal waste. Not a mousetrap. Got regulatory approval. Good characteristics. Terrible P&L but increasing revenues. $10 billion TAM dominated by waste haulers. That was Aug 2005.

Later in Oct 2005, I said that their P&L was terrible and revenues were actually shrinking.

Ok, let's see what happened. Q3 10-Q for period ending June 30, 2006 shows increasing revenues again (although not all that much for 9 months). They still have a massive operating loss much greater than revenues. Balance sheet is solid with big net cash (of course they issued a big chunk of convertable preferred stock to raise a ton of cash). Cash flow is terrible.

Ok, so how about the stock price? Down from about $2.00 to about 60 cents.

Grade: easy A

QBID

Ok, so I always considered this a horrible company and they proved me right by going bankrupt and issuing a joke of a financial statement (gone now).

Grade: easy A

CCCI (stock, old sec)

First looked at it here. In the China cable TV market, they were in a great starting location, but they only had hopes of success. I know that TV is big in China. But I stopped following the company here due to huge losses and terrible balance sheet. They ended up going AWOL, Pink Sheets can't find them. No news. Stock is selling for about half a cent. Their website expired. Only 3K shares shorted. I wasn't fooled by stuff like this.

Grade: easy A

MANS (stock, sec)

First looked at it here in August 2005. First looked at it here. I said they were a mousetrap and serial acquirer. They claimed to be "focusing" on being a leader, but they weren't and were losing money to boot.

Ok, so how are they doing now? They just got a new CFO. Dismissed the auditors.

10-K for period ending June 30, 2006:

New CEO. Private placement (tough terms?).

They bought the assets of ITF Optical Technologies in April 2006 for cash and stock. Serial acquirer? Check! Although they were very closely intertwined with MANS.

Risk Factor 1:

Ok, so how about the stock price? Long slow decline. Currently 24 cents at the ask. Was about 40 cents when I first looked at it.

Grade: easy A

5/28/2006 Checking back with Mr. Market: 1

BFTC, LIAL, LCLG, BRSI, BSOG, BAYN, RCBK, CNB, CFNA, WTFC, Pacific International Bank, BGII, BLYM, AMEN, BVBC, BNSIA, BOGN, BONL, BAWC, BWTL, BPTR, BDLF, BLLD, BURCA, LVWD, BKBO, BOJF, SCCB

5/29/2006 Checking back with Mr. Market: 2

BUKS, XAIN, YIWA, SHFK, SODI, YHGG

10/13/2006 Results 1

BFTC, BKBO, LVWD, LCLG, BRSI, BSPA, BSOG, BOJF, BAYN (Oops, I already did these!)

10/21/2006 Results 2

ADY, BABB, BACL, CACC

New Results:

CBBT (now CBAK, sec)

First looked at it here. My notes only say that it wasn't cheap at the time. It's selling today for around the same price: $6.66.

Here's something you don't see very often: stock options cancelled at the request of the employees.

The optionees requested the Company to terminate their options, so that they could avoid adverse tax consequences under applicable Chinese law.A patent infringement lawsuit was filed against CBAK. Conference call transcript for Q3 2006 results. Revenues down:

Hindsight always being 20/20, we conducted a detailed postmortem on the quarter. Historically, BAK had always found itself with more potential demand than we had the manufacturing capacity to serve. So in previous years, we only felt a very minor impact from a seasonal slowdown that occurs in our businesses between April and July. In 2006, we entered the quarter with ample capacity of 22 million per month and therefore, felt the full impact of this year’s seasonal decline in demand.10-Q for period ending June 30, 2006. AR up, inventories up, PP&E way up. Reasonable balance sheet. Gross margins aren't so great for the business, but operating margins are ok. Earned 9 cents diluted (31 cents for 9 months). Operating cash flow bad due to AR and inventories. Was great last year. Huge capex above depreciation (I seem to recall they're in investment mode). Some net borrowing.

I’d like to point out that we did not lose any customers and we did not experience any work stoppages or suspension of production from quality issues. We do not believe that we lost any market share. Our customers simply sold less due to a general seasonal slowdown and in turn, they ordered less from us.

Another reason behind the drop in demand is that we believe that our customers reduced their inventories over the past few months. In the past our capacity and therefore our flexibility to ship additional orders or to react to emergency shipments was extremely limited. This was due to our limited capacity. We believe that our customers, therefore, protected themselves by maintaining a safety stock of our products in their inventory.

So far, I'd say that I called this one reasonably well (although the stock is down because they've had a bigger than expected slowdown).

Grade: B

CAPS (stock, sec)

First looked at it here. Neutralizing medical waste into normal waste. Not a mousetrap. Got regulatory approval. Good characteristics. Terrible P&L but increasing revenues. $10 billion TAM dominated by waste haulers. That was Aug 2005.

Later in Oct 2005, I said that their P&L was terrible and revenues were actually shrinking.

Ok, let's see what happened. Q3 10-Q for period ending June 30, 2006 shows increasing revenues again (although not all that much for 9 months). They still have a massive operating loss much greater than revenues. Balance sheet is solid with big net cash (of course they issued a big chunk of convertable preferred stock to raise a ton of cash). Cash flow is terrible.

Ok, so how about the stock price? Down from about $2.00 to about 60 cents.

Grade: easy A

QBID

Ok, so I always considered this a horrible company and they proved me right by going bankrupt and issuing a joke of a financial statement (gone now).

Grade: easy A

CCCI (stock, old sec)

First looked at it here. In the China cable TV market, they were in a great starting location, but they only had hopes of success. I know that TV is big in China. But I stopped following the company here due to huge losses and terrible balance sheet. They ended up going AWOL, Pink Sheets can't find them. No news. Stock is selling for about half a cent. Their website expired. Only 3K shares shorted. I wasn't fooled by stuff like this.

Grade: easy A

MANS (stock, sec)

First looked at it here in August 2005. First looked at it here. I said they were a mousetrap and serial acquirer. They claimed to be "focusing" on being a leader, but they weren't and were losing money to boot.

Ok, so how are they doing now? They just got a new CFO. Dismissed the auditors.

10-K for period ending June 30, 2006:

New CEO. Private placement (tough terms?).

They bought the assets of ITF Optical Technologies in April 2006 for cash and stock. Serial acquirer? Check! Although they were very closely intertwined with MANS.

Risk Factor 1:

There exists substantial doubt about our ability to continue as a going concernTo be fair, revenues nearly tripled during the last year (due more than entirely to their acquisition). Gross profit went up to $3 million from $1.3 million! However, operating expenses went up from $6.3 million to $11 million. Goodwill and other intangible impairment.

Ok, so how about the stock price? Long slow decline. Currently 24 cents at the ask. Was about 40 cents when I first looked at it.

Grade: easy A

Monday, November 06, 2006

Chinese Real Estate Law

This paper, Acquiring Land Use Rights in Today's China: A Snapshot From the Ground, written by Gregory M. Stein, a law professor at the University of Tennessee, takes a pragmatic view of what's going on in Chinese real estate, especially in Shanghai (supposedly one out of every five of the world's construction cranes are there). It's based on first-hand interviews with about 50 people who are directly involved in the industry.

Some key points to take away:

Nothing is time-tested. There are no seasoned experts in the field. The most experienced people have been at it for not much more than a decade; they've only experienced boom times. As an interesting similar example, most Chinese people driving cars today haven't been driving for very long at all and have the driving experience of a Western teenager, regardless of their actual age.

Legal changes are often incremental and only dealing with the immediate needs rather than stepping back and solving the overall abstract issues.

Even with the free markets and relaxed regulations, the Chinese legal system still has a lot more "government involvement, intrusion, and interference than American real estate professionals typically experience."

The background history section has an interesting quote:

Within the Shanghai area, China built a city the size of Chicago in less than 15 years.

Very often a local government entity will own part of the land use rights jointly with a limited liability company. It then "uses that control to gain an ownership interest in the entity that will develop the land." In theory, they aren't supposed to profit from the activities after 1990. Sometimes, state-owned enterprises (SOEs) have land use rights from local governments and then contribute these to a jointly owned development entity.

In the very early real estate market, SOEs or the government were the only players with any expertise.

The government's dealings with land use rights seem to be far from arm's length. Some land use rights are sold for far less than they're worth [which is often difficult to objectively know ahead of time] and the purchaser can resell parts of it for a profit and then continue with a project with essentially free land use rights. This might often be associated with "connections" with the right people.

The government entities hold the land use rights but often don't have the development expertise. The developers willing to "share the spoils" with the government or certain members of the government can get the deals. In other cases, the corruption is more subtle. Multiple sources indicate that the city of Shanghai uses land use auctions which are now very clean and transparent. However, good connections are likely to remain critical for the foreseeable future. And the people who get established early are likely to retain a competitive edge after things get more transparent. Very often those people are the ones who push for clean rules to keep others from playing the same tricks going forward. [Someone argued that this is what the US is doing globally]

It sounds a lot like your basic "local corruption" state of affairs that you'd find in some seedier out-of-the way parts of the US.

Not too many years ago, developers paid contractors slowly, forcing them to extend interest-free loans and assume some of the risk if the project failed (again, sounds like the usual bag-of-tricks in seedier untransparent dealings in the US). The government has been cracking down on this to slow the overheated expansion. But contractors figured a way around it.

Humorous quote:

Apparently, the only example of a citizen's input into any aspect of land use planning was due to a 12 year old girl's suggestion for the 360+ degree circular exit ramp on the Nanpu Bridge in Shanghai (I recall seeing that 8 years ago on the cover of an engineering book here). Generally, the government does whatever it wants without citizen input, 12 year old bridge designers not withstanding.

Obviously it's in the local governments' best interests to increase development to generate revenue from land use rights and taxation on the resulting businesses. The central government has reasons to want to avoid property booms and to preserve agricultural land (peasant revolts, strategic food supplies).

Residential property land rights can go up to 70 years.

Commercial property land rights can go up to 40 years.

Industrial property rights up to 50 years.

[the residential being green, commercial being purple, and industrial being yellow for those who remember their Sim City games]

There's a 2 year use-it-or-lose it requirement that is often ignored or modified. There may be restrictions of all sorts placed on the land rights.

Land use rights are paid entirely in advance, some say you can't borrow money for this (although that would be hard to rigorously enforce, I'd imagine). Landlord-tenant law doesn't apply.

After expiration, it's difficult to know what exactly will happen in most cases, especially since the laws are so new. But in short-term cases that are expiring soon, the government seems to be willing to negotiate an extension or else compensated for the buildings it is now taking possession of. Over time, it may be that land use rights transform into something like Western ground leases or else something like Western property taxes in the US.

Municipalities use land use rights to keep a flow of revenues. It all strikes me a lot like a giant game of Sim City.

Some key points to take away:

China's legal system is developing so rapidly that the few [written] sources that exist are obsolete almost immediately.... Those Chinese citizens who have developed expertise in the emerging legal and business systems of China are more apt to be profiting from it than writing treatises about it.A lot of the experts he dealt with were curious to see what he learned so they could get more overall knowledge themselves. The National People's Congress is still debating the nation's first comprehensive property code. This debate is exposing serious ideological splits within the Chinese Communist Party.

Nothing is time-tested. There are no seasoned experts in the field. The most experienced people have been at it for not much more than a decade; they've only experienced boom times. As an interesting similar example, most Chinese people driving cars today haven't been driving for very long at all and have the driving experience of a Western teenager, regardless of their actual age.

...the Chinese legal system is surpisingly undeveloped given how advanced the Chinese property markets have become. A casual observer viewing Shanghai's skyline for the first time would assume that Chinese property law has matured significantly since Mao's death, but this assumption is only partly correct.It's sounds a lot like how rules and regulations regarding Internet activities have rapidly evolved chaotically and have always lagged behind the actual activities themselves.

The legal systems is far from transparent, enforcement of the laws that are on the books is inconsistent and commonly graft-ridden, and the rule of law is viewed as a Western concept that does not interlock well with Chinese traditions.There is a lot more reliance on personal relationships than in the West. There's a big gap between the laws on the books and how law is practiced. The results of anyone's actions may be difficult to predict.

Legal changes are often incremental and only dealing with the immediate needs rather than stepping back and solving the overall abstract issues.

Even with the free markets and relaxed regulations, the Chinese legal system still has a lot more "government involvement, intrusion, and interference than American real estate professionals typically experience."

The background history section has an interesting quote:

Show me a Chinese centenarian and I will show you a person who has lived through unbelievable change in her lifetime. She will have been born in the waning days of the Qing Dynasty, with the Last Emperor soon to succumb to the republican revolution of 1911. A quarter-century of upheaval followed, marked by four years of a shaky republic, twelve years of regional control by warlords, and the establishment of the Nationalist government in 1928, alongside the growth of the Communist Party. Nationalist control of much of China would gradually give way to invading forces from Japan [often very brutal and for nearly a decade].... Four years of uncertainty and civil war would follow the departure of the Japanese. Then would come the quarter-century of Mao Zedong's rule, difficult and often brutal years marked ultimately by the nationalization of all land in China.Then there was the era of Deng Xiaoping, with the emerging market based economy and huge improvements in the standard of living for large numbers of Chinese. The creation of transferable land use rights was in 1988. The Land Administration Law was adopted in 1986 and revised in 1998.

Within the Shanghai area, China built a city the size of Chicago in less than 15 years.

Very often a local government entity will own part of the land use rights jointly with a limited liability company. It then "uses that control to gain an ownership interest in the entity that will develop the land." In theory, they aren't supposed to profit from the activities after 1990. Sometimes, state-owned enterprises (SOEs) have land use rights from local governments and then contribute these to a jointly owned development entity.

In the very early real estate market, SOEs or the government were the only players with any expertise.

The government's dealings with land use rights seem to be far from arm's length. Some land use rights are sold for far less than they're worth [which is often difficult to objectively know ahead of time] and the purchaser can resell parts of it for a profit and then continue with a project with essentially free land use rights. This might often be associated with "connections" with the right people.

The government entities hold the land use rights but often don't have the development expertise. The developers willing to "share the spoils" with the government or certain members of the government can get the deals. In other cases, the corruption is more subtle. Multiple sources indicate that the city of Shanghai uses land use auctions which are now very clean and transparent. However, good connections are likely to remain critical for the foreseeable future. And the people who get established early are likely to retain a competitive edge after things get more transparent. Very often those people are the ones who push for clean rules to keep others from playing the same tricks going forward. [Someone argued that this is what the US is doing globally]

It sounds a lot like your basic "local corruption" state of affairs that you'd find in some seedier out-of-the way parts of the US.

Not too many years ago, developers paid contractors slowly, forcing them to extend interest-free loans and assume some of the risk if the project failed (again, sounds like the usual bag-of-tricks in seedier untransparent dealings in the US). The government has been cracking down on this to slow the overheated expansion. But contractors figured a way around it.

Humorous quote:

The developers I interviewed generally wish to make money and seemed a bit surprised that an American would see any need to ask a Chinese developer about this.Academic people are such a riot.

Apparently, the only example of a citizen's input into any aspect of land use planning was due to a 12 year old girl's suggestion for the 360+ degree circular exit ramp on the Nanpu Bridge in Shanghai (I recall seeing that 8 years ago on the cover of an engineering book here). Generally, the government does whatever it wants without citizen input, 12 year old bridge designers not withstanding.

Obviously it's in the local governments' best interests to increase development to generate revenue from land use rights and taxation on the resulting businesses. The central government has reasons to want to avoid property booms and to preserve agricultural land (peasant revolts, strategic food supplies).

Residential property land rights can go up to 70 years.

Commercial property land rights can go up to 40 years.

Industrial property rights up to 50 years.

[the residential being green, commercial being purple, and industrial being yellow for those who remember their Sim City games]

There's a 2 year use-it-or-lose it requirement that is often ignored or modified. There may be restrictions of all sorts placed on the land rights.

Land use rights are paid entirely in advance, some say you can't borrow money for this (although that would be hard to rigorously enforce, I'd imagine). Landlord-tenant law doesn't apply.

After expiration, it's difficult to know what exactly will happen in most cases, especially since the laws are so new. But in short-term cases that are expiring soon, the government seems to be willing to negotiate an extension or else compensated for the buildings it is now taking possession of. Over time, it may be that land use rights transform into something like Western ground leases or else something like Western property taxes in the US.

Municipalities use land use rights to keep a flow of revenues. It all strikes me a lot like a giant game of Sim City.

Thursday, November 02, 2006

Strathmore (STM.V, STHJF) stakes another claim

Strathmore Minerals (combined links) issued a press release today.

Gas Hills Uranium District in Wyoming. 45 miles east of Riverton. Looks like it's in the Teton National Forest. Good luck with permitting, even if Dave Miller is in the Wyoming legislature.

Roll front deposits in sandstone (hopefully very porous) between shales and mudstones making ISR* likely. Uranium trend at 300 feet deep found at the property boundary. Some exploration done in the 70s and 80s. Recall that Strathmore owns a large amount of database records.

Notable infrastructure exists on the property: haulage roads, electrical power lines (presumably usable?). Looks like they plan about 60 drill holes after getting a permit. They already started the eco studies (archeology/flora/fauna) assuming they get mining permitting on the property.

* everyone seems to be calling ISL (in situ leaching) mining ISR (in situ recovery) mining lately, probably to make it sound better (like how they changed nuclear magnetic resonance spectroscopy to just magnetic resonance spectroscopy to keep the Church of Latter Day Environmentalists from false witch hunting). In reality the "leaching" uses acids or bases about as caustic as baking soda or vinegar and it's all extracted back out.

Gas Hills Uranium District in Wyoming. 45 miles east of Riverton. Looks like it's in the Teton National Forest. Good luck with permitting, even if Dave Miller is in the Wyoming legislature.

Roll front deposits in sandstone (hopefully very porous) between shales and mudstones making ISR* likely. Uranium trend at 300 feet deep found at the property boundary. Some exploration done in the 70s and 80s. Recall that Strathmore owns a large amount of database records.

Notable infrastructure exists on the property: haulage roads, electrical power lines (presumably usable?). Looks like they plan about 60 drill holes after getting a permit. They already started the eco studies (archeology/flora/fauna) assuming they get mining permitting on the property.

* everyone seems to be calling ISL (in situ leaching) mining ISR (in situ recovery) mining lately, probably to make it sound better (like how they changed nuclear magnetic resonance spectroscopy to just magnetic resonance spectroscopy to keep the Church of Latter Day Environmentalists from false witch hunting). In reality the "leaching" uses acids or bases about as caustic as baking soda or vinegar and it's all extracted back out.

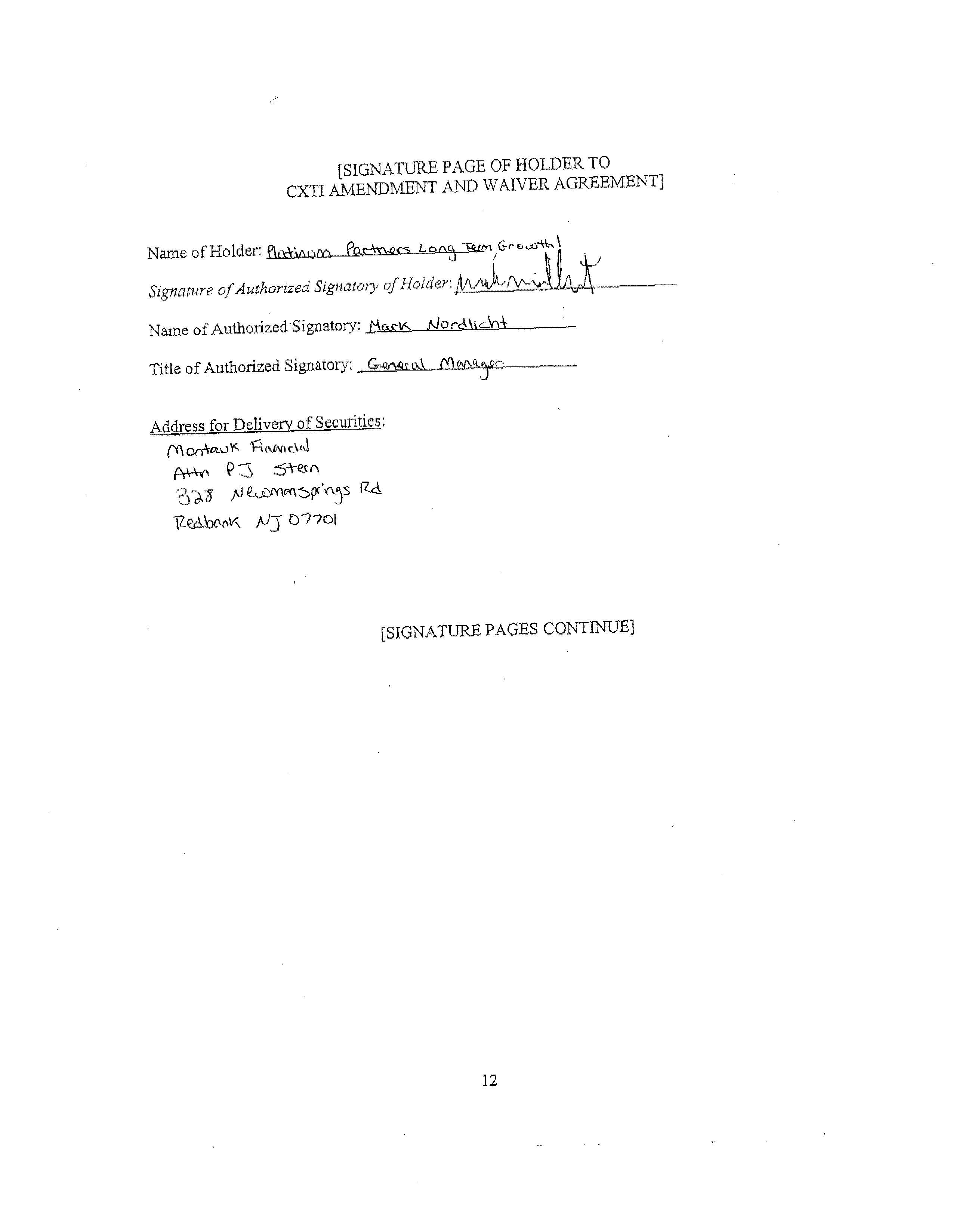

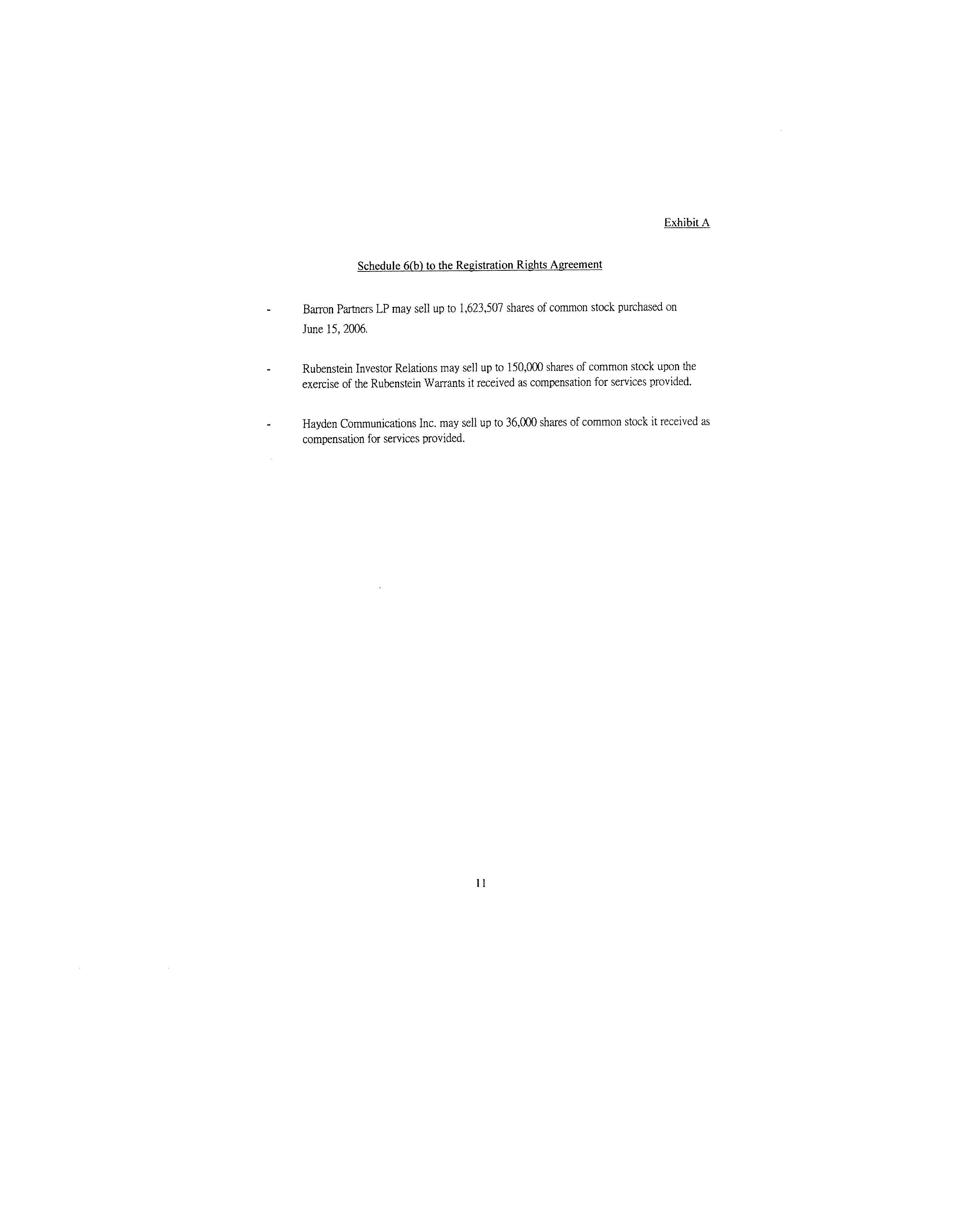

China Expert Technologies (CXTI) makes agreement with debenture holders

CXTI (combined links) press release.

The debenture holders ("Holders"):

Alpha Capital AG, DKR Soundshore Oasis Holding Fund, Ltd., Ellis International, Platinum Partners Advisors, LLC, and Platinum Long Term Growth I, LLC

$6 million face amount, 7% "toxic" convertibles, due/payable on Halloween 2006. Some was converted. $4.4 million remained. The Holders have the right to extend the due date to April 30, 2007, no interest. All of them chose to extend. Detoxified. Conversion price fixed at $1.80, which is what they almost certainly would have gotten anyway, given the stock price, business performance, and previous terms.

CXTI defaulted by failing to get a registration statement effective 200 days after the deal was made last Halloween. The Holders agreed to accept payment for damages of 614K shares of restricted stock. The Holders waive other rights and remedies. Here's the damage allocation.

The overall amendment. One of the signatures is from "Platinum Partners Long Term Growth".

Various Holders are entitled to sell about 1.8 million shares.

Here's the original agreement. Section 8 deals with defaults. Paragraph a) ix deals with the 200 day limit on the registration statement. Subsection b) deals with remedies upon default. The principal and accrued interest is due immediately if elected by the Holders [yeah, I know, I'm mixing definitions from two different contracts]. Payable in stock at what would be $1.80 for a total of at least $1 meeellion dollars, or 556K shares. So they got an extra $100K?

I continue to own the stock.

UPDATE Nov 3, 2006:

Lecontinental is correct, even my own notes here show only two debenture holders remaining.

The debenture holders ("Holders"):

Alpha Capital AG, DKR Soundshore Oasis Holding Fund, Ltd., Ellis International, Platinum Partners Advisors, LLC, and Platinum Long Term Growth I, LLC

$6 million face amount, 7% "toxic" convertibles, due/payable on Halloween 2006. Some was converted. $4.4 million remained. The Holders have the right to extend the due date to April 30, 2007, no interest. All of them chose to extend. Detoxified. Conversion price fixed at $1.80, which is what they almost certainly would have gotten anyway, given the stock price, business performance, and previous terms.

CXTI defaulted by failing to get a registration statement effective 200 days after the deal was made last Halloween. The Holders agreed to accept payment for damages of 614K shares of restricted stock. The Holders waive other rights and remedies. Here's the damage allocation.

{kind=link}

The overall amendment. One of the signatures is from "Platinum Partners Long Term Growth".

{kind=link}

Various Holders are entitled to sell about 1.8 million shares.

{kind=link}

Here's the original agreement. Section 8 deals with defaults. Paragraph a) ix deals with the 200 day limit on the registration statement. Subsection b) deals with remedies upon default. The principal and accrued interest is due immediately if elected by the Holders [yeah, I know, I'm mixing definitions from two different contracts]. Payable in stock at what would be $1.80 for a total of at least $1 meeellion dollars, or 556K shares. So they got an extra $100K?

CONCLUSION

I'm not sure why CXTI didn't get the registration in time. Maybe there were hoops that they couldn't jump in time. But I also wonder why the Holders accepted the extension. Perhaps they're interested in the company's long term value? I don't know.I continue to own the stock.

UPDATE Nov 3, 2006:

Lecontinental is correct, even my own notes here show only two debenture holders remaining.

Epolin (EPLN)

Epolin (combined links) filed an 8-K this week saying that the Chairman, Murray S. Cohen, will take a 50% pay cut in base salary because he's partially retired. I assume this means the new CEO, Greg Amato, is doing OK.

Based on the latest proxy, Cohen's salary was $305K for last year, this adds $152K to the income. In the 10-K, net income was $594K for the year ending Feb 28, 2006. If you take taxes into account, the pay cut adds $96K or 16% to the bottom line.

Based on the latest proxy, Cohen's salary was $305K for last year, this adds $152K to the income. In the 10-K, net income was $594K for the year ending Feb 28, 2006. If you take taxes into account, the pay cut adds $96K or 16% to the bottom line.

![]()